South Carolina Property Tax Records and Assessment Data

South Carolina property tax records are maintained at the county level and provide key details about assessed values, tax bills, ownership history, and payment status. Each of the state's 46 counties operates its own assessor, auditor, and treasurer offices to handle property tax functions. Whether you need to verify a tax assessment, look up a parcel's tax history, or confirm that taxes are current on a piece of real estate, this guide explains how to find and use South Carolina property tax records through official county and state sources.

South Carolina Property Tax Quick Facts

How South Carolina Property Taxes Work

South Carolina uses an ad valorem property tax system. That means taxes are based on the value of the property. Three separate county offices handle different parts of the process. The county assessor determines the fair market value of real property. The county auditor then applies the appropriate assessment ratio and millage rate to calculate the tax bill. The county treasurer collects the tax payments and manages delinquencies. This three-office structure is used across all 46 South Carolina counties.

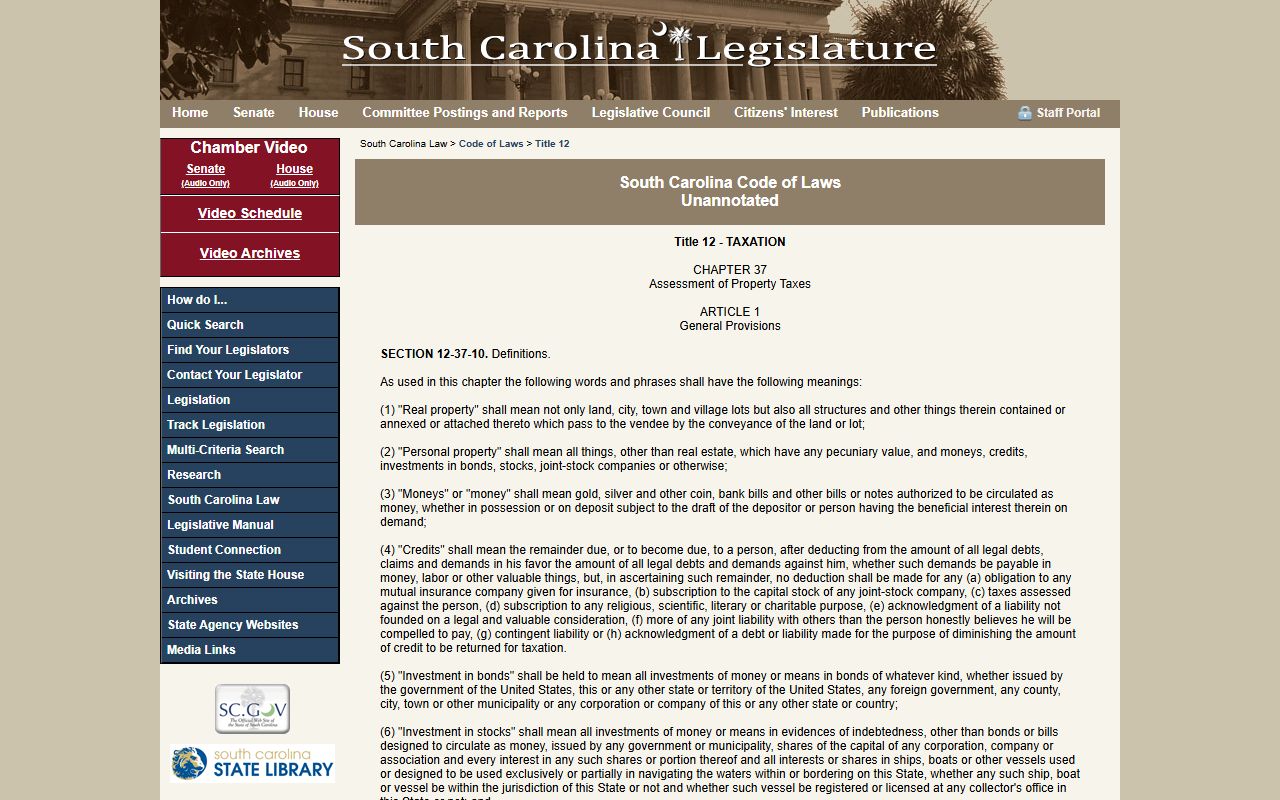

Under SC Code Section 12-37-10, real property includes land, city and town lots, and structures attached to the land. Personal property covers everything else that holds monetary value. The county assessor is responsible for maintaining deed and sales records, tracking building permits, managing tax maps, discovering unlisted property, and reappraising values when changes occur. South Carolina law under Section 12-37-90 requires every county to employ a full-time assessor to carry out these duties. The assessor's office is the first place to go when searching property tax records in South Carolina.

The South Carolina Association of Counties coordinates services across all 46 counties and supports county officials in carrying out tax administration duties. The state's median effective property tax rate is 0.72%, which is well below the national median of 1.02%. Rates vary by county, ranging from around 0.35% in Horry County to approximately 0.74% in Richland County. Under SC Code Section 12-37-30, all taxes must be levied on a uniform basis of assessment across the state.

The South Carolina Department of Revenue oversees statewide tax policy and provides guidance on property tax rules, including the MyDORWAY portal, published revenue rulings, and support for taxpayers navigating assessment questions.

South Carolina Property Tax Assessment Ratios

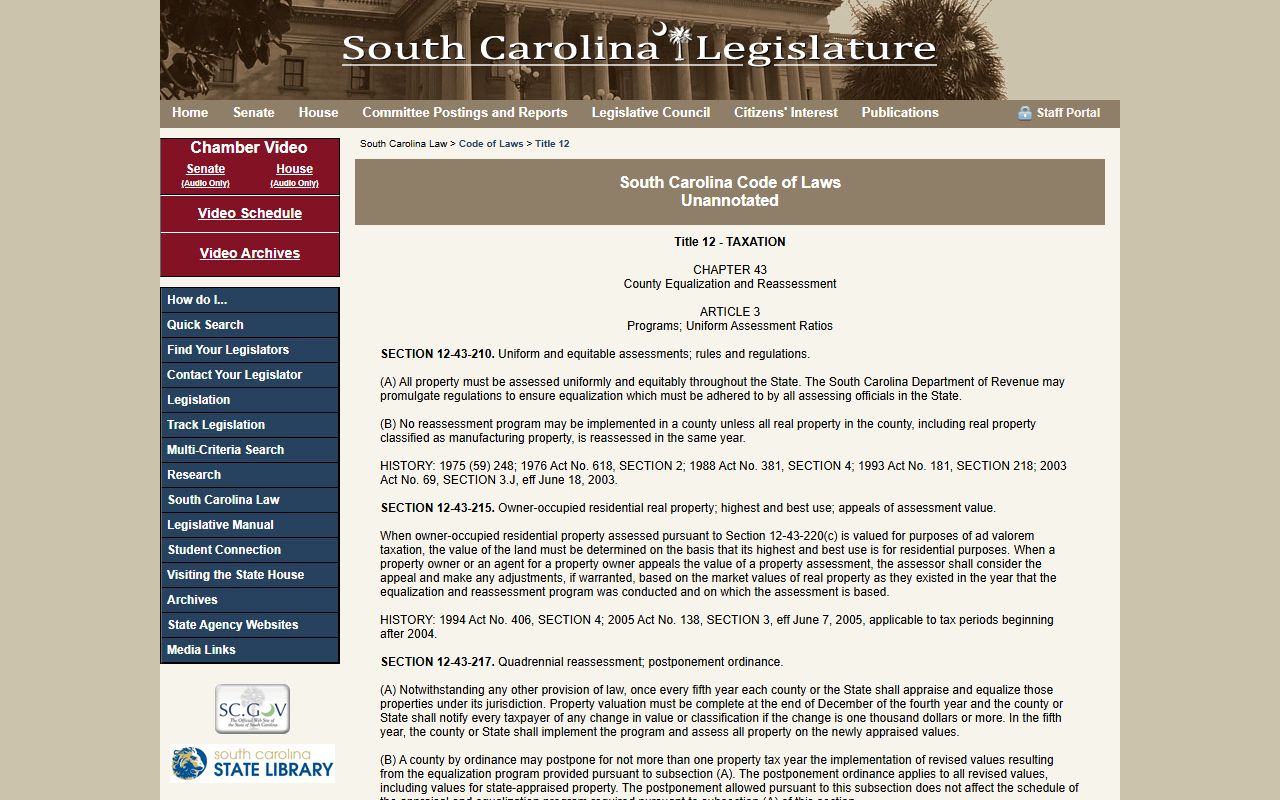

Not all property is taxed at the same percentage of its fair market value. South Carolina law sets specific assessment ratios for different property types. These ratios determine how much of a property's value is subject to the millage rate applied by the local taxing authority. Under SC Code Section 12-43-220, the ratio for an owner-occupied legal residence is 4%, applied to properties of five contiguous acres or less. Agricultural property owned by private individuals is also assessed at 4%. Corporate-owned agricultural land carries a 6% ratio. Commercial real property is assessed at 6%. Manufacturing property is taxed at 10.5%, the same rate applied to most other personal property.

The 4% legal residence rate is the most valuable tax benefit available to South Carolina homeowners. It applies only when the property is the owner's primary residence. To qualify, the owner must apply through the county assessor's office and show that the home is their principal place of residence. Properties that do not qualify default to the 6% rate. Many homeowners are unaware they must actively apply for this designation. Failing to do so can mean a substantially higher annual tax bill.

The difference matters. A home assessed at $300,000 carries a taxable base of $12,000 at the 4% ratio. That same home at 6% carries a $18,000 taxable base before the millage rate is applied. Owners of multiple properties in South Carolina may only claim the 4% ratio on one property.

SC Code Title 12 contains all state tax laws, including the chapters governing property assessment ratios, equalization schedules, collection deadlines, delinquency procedures, and appeal rights for South Carolina property owners.

Note: Owners of multiple properties in South Carolina may only claim the 4% legal residence ratio on one property, since it must be their primary home.

Finding South Carolina Property Tax Records Online

Most South Carolina counties provide online access to property tax records through their assessor or treasurer websites. Many counties use the qPublic platform, which allows users to search by owner name, parcel number, or property address. Results typically include assessed value, fair market value, tax district, millage rate, and current tax status. Some counties also offer GIS mapping tools that display parcels visually alongside assessment data. These tools are free to use and available around the clock.

For property-specific records, the county is always the primary source. Each county assessor maintains a database of all real property within its boundaries. Deed and sales data, building permit records, and tax maps are all part of the assessor's required recordkeeping under state law. Most of these records are accessible without a visit to a government office. Searching by parcel ID or owner name through the county's online portal is the quickest method for locating South Carolina property tax records.

Chapter 37 of SC Code Title 12 defines real and personal property, establishes the duties of county assessors, and sets the rules for maintaining tax records, discovering unlisted property, and reappraising values across South Carolina.

South Carolina Property Tax Exemptions

South Carolina provides several property tax exemptions that reduce or eliminate tax liability for qualifying owners. The most widely used is the Homestead Exemption, which exempts the first $50,000 of fair market value for qualifying homeowners. To be eligible, the owner must be age 65 or older, totally and permanently disabled, or legally blind. They must hold fee simple title to the property for at least one year. Applications go through the county auditor's office, not the assessor. The exemption applies to county, municipal, and most school taxes.

Other exemptions under SC Code Section 12-37-220 cover a range of property types. Property owned by the state or its political subdivisions is exempt from property taxes. So is property used for schools, colleges, and churches. Household goods used in the home, agricultural products held for sale, farm buildings used for agricultural purposes, and livestock all qualify for exemption under state law. These exemptions apply statewide and cannot be limited by local ordinance.

Manufacturers may also benefit from special assessment rules. Under SC Revenue Ruling 16-12, manufacturers submit returns to the Department of Revenue, with assessment based on returns filed by the fourth month after the accounting period closes. This places manufacturing property assessment at 10.5% of value under Section 12-43-220.

Chapter 43 governs the equalization and reassessment of property values across South Carolina's 46 counties, establishing uniform assessment practices and the statewide five-year reappraisal schedule.

South Carolina Property Tax Due Dates and Penalties

South Carolina property tax bills are mailed in the fall each year. Under SC Code Section 12-45-70, taxes are due between September 30 and January 15 of the following year. January 15 is the key deadline for most owners. Missing that date triggers a 3% penalty starting January 16. An additional 7% penalty applies after February 2. A further 5% penalty is added after March 16. These penalties are cumulative, so delays past the first deadline compound quickly.

Some counties offer installment payment plans under Section 12-45-75, allowing owners to spread payments across several months before the January 15 deadline. This option helps owners avoid a single large payment. For those who pay by mail, the US postmark date determines timeliness under Section 12-45-180. A payment postmarked by January 15 is considered on time even if the county receives it after that date. Keep your mailing receipt when paying close to the deadline.

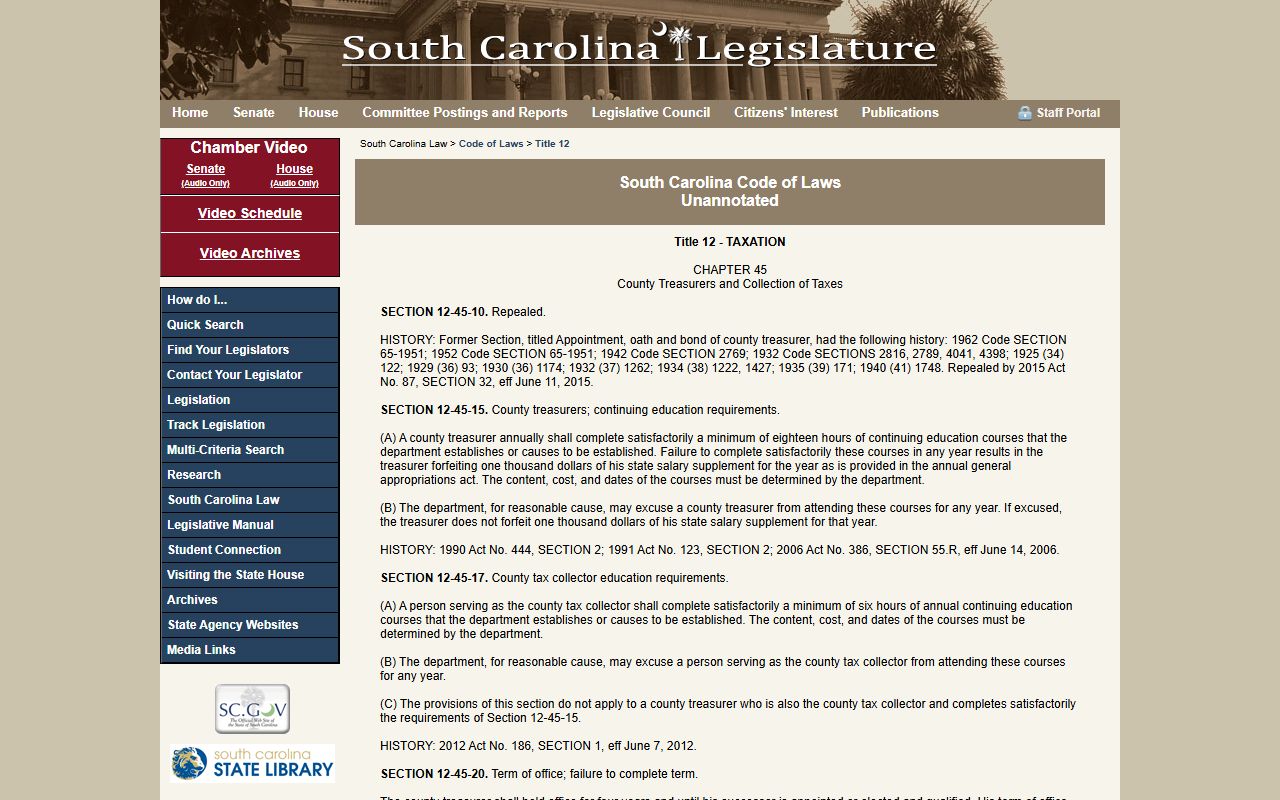

Chapter 45 sets the rules for county treasurers collecting property taxes, covering payment due dates, penalty schedules, installment options, and the postmark rule for mailed payments.

Note: South Carolina property tax bills are paid in arrears, meaning the bill you receive in the fall covers taxes for that same calendar year and is due by January 15 of the following year.

How South Carolina Property Reassessment Works

South Carolina law requires that all real property be reappraised and equalized on a consistent schedule. Under SC Code Section 12-43-217, each county must complete a full reassessment every five years. The reappraisal must be finished by the end of December in the fourth year of the cycle. This uniform statewide schedule keeps assessed values aligned with actual market conditions and prevents values from drifting far from current prices over time.

When a county completes a reassessment, property values may rise or fall based on real estate market trends. South Carolina includes a reassessment cap provision that limits the tax impact of value increases in certain cases. If a reassessment would cause a tax increase solely because of higher market values, the millage rate may be adjusted to offset that increase. This mechanism protects owners from automatic tax hikes triggered purely by rising market values.

Keeping track of your county's reassessment year matters. Review your assessment notice carefully when one arrives. Values listed on older records may not reflect the current assessed value after a reassessment cycle has been completed. Many county assessor websites display the year of the last reappraisal and the current assessed value for each parcel in the county's database.

Delinquent South Carolina Property Tax Records

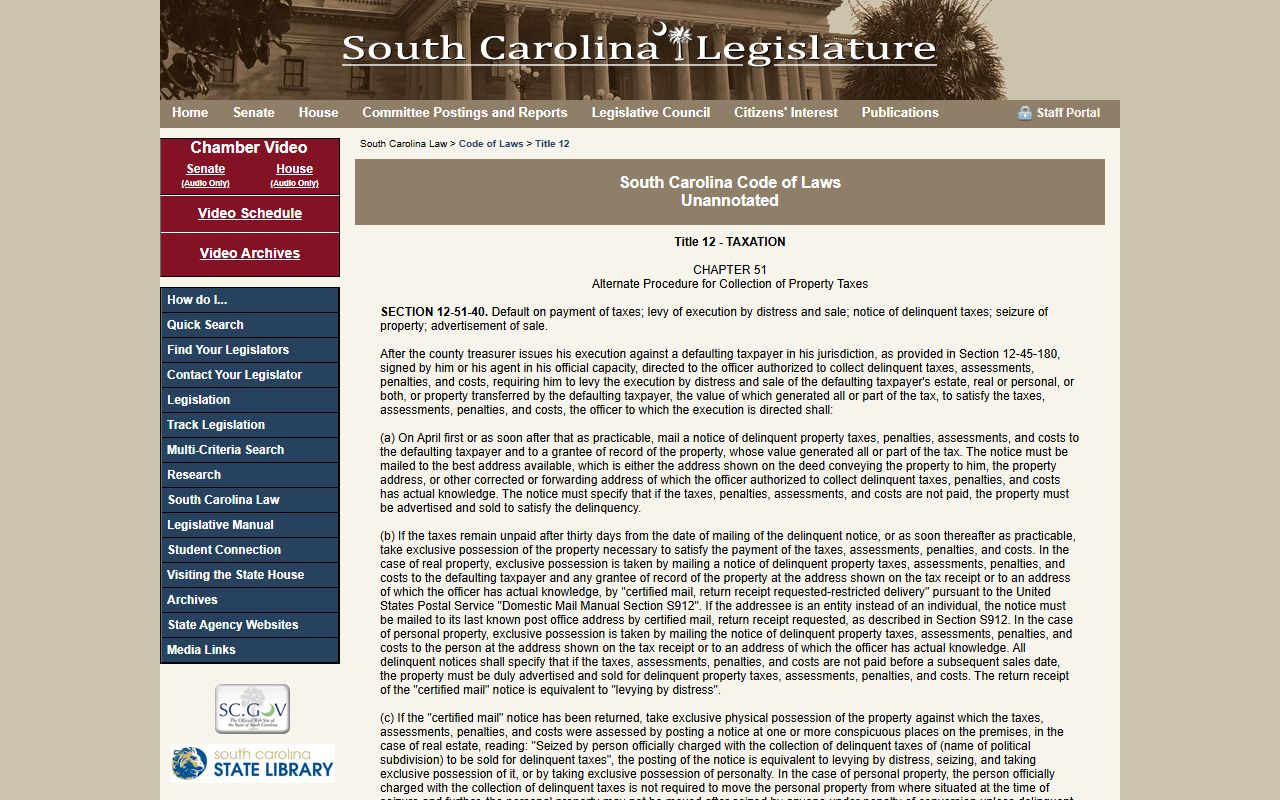

When property taxes go unpaid past the January due date, the county begins a formal delinquency process. Under SC Code Section 12-51-40, the county must mail a delinquency notice by April 1. If taxes remain unpaid for 30 or more days after that notice, the county must follow up by certified mail or by posting notice on the property. Before any tax sale can occur, the delinquency must be advertised in a local newspaper for three consecutive weeks. These steps are required by law and cannot be skipped.

Chapter 51 outlines the complete delinquent property tax collection process in South Carolina, from initial notice through tax sale and the 12-month redemption period available to original owners after a sale.

After a tax sale, the original owner has a 12-month redemption period under Section 12-51-90 to reclaim the property. Doing so requires paying the outstanding taxes plus accrued interest. Interest rates increase over the redemption period: 3% for months one through three, 6% for months four through six, 9% for months seven through nine, and 12% for months ten through twelve. Delinquent tax records are public and available through county treasurer offices or their online portals. Under SC Code Section 12-49-10, property taxes are the first lien on a property in all cases. The lien attaches on December 31 for the following year's taxes under Section 12-49-20.

Appealing a South Carolina Property Tax Assessment

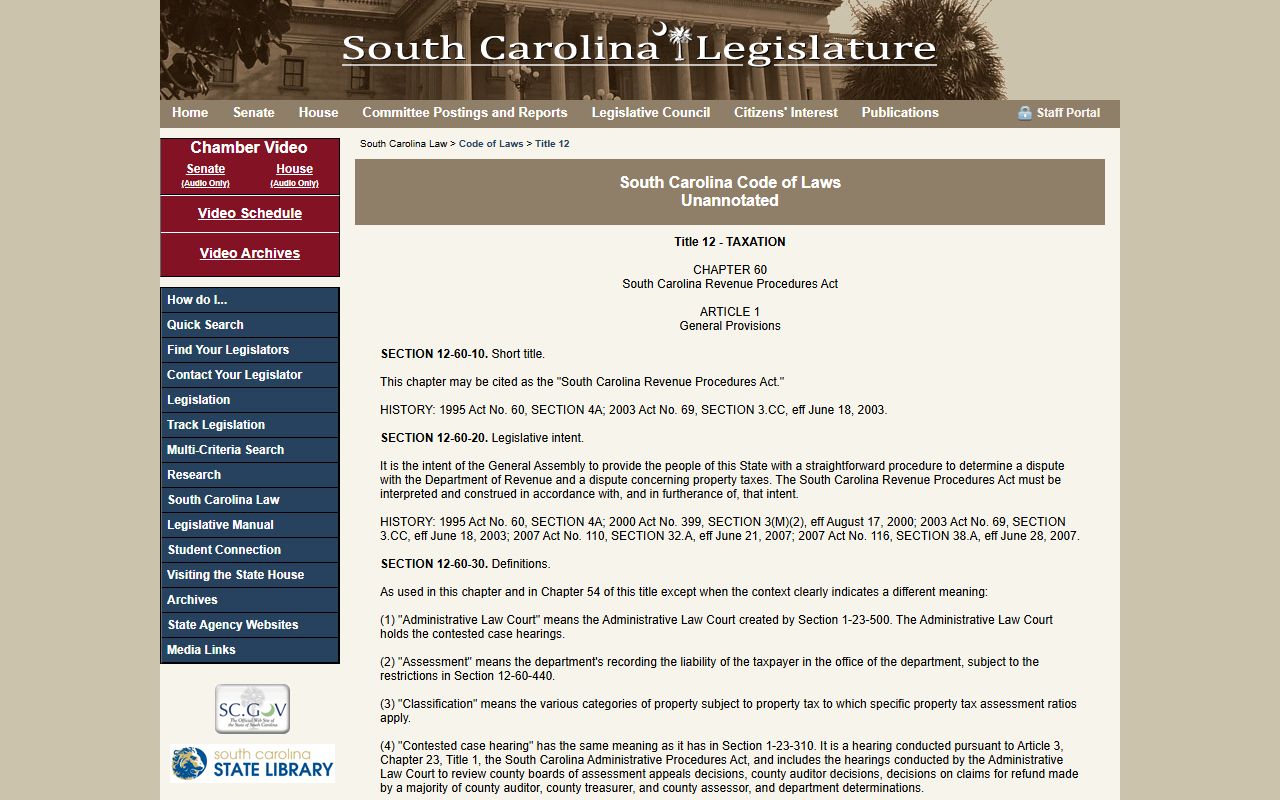

Property owners who disagree with their assessed value or property classification have the right to appeal. SC Code Section 12-60-20 describes the state's intent to provide a straightforward procedure for resolving property tax disputes. The process starts at the county assessor's office. The owner must file a written objection within a specified number of days after receiving the assessment notice. Waiting past that window typically closes the appeal option for that year.

Chapter 60 establishes the revenue procedures and appeal rights available to South Carolina property owners who contest their tax assessment, including the path to an Administrative Law Court hearing.

If the assessor does not resolve the dispute to the owner's satisfaction, the case can proceed to a county board of assessment appeals. From there, unresolved cases may advance to the Administrative Law Court for a contested case hearing. Owners must exhaust all prehearing remedies before bringing a case to that court level. Supporting documentation strengthens any appeal. Recent appraisals, comparable sales data, and photos documenting property condition are all useful. Many counties now allow owners to submit this material online when filing their initial objection to a South Carolina property tax assessment.

The South Carolina Association of Counties serves all 46 county governments through legislative advocacy, coordination, and education for county officials who administer property taxes and maintain property tax records across the state.

Browse South Carolina Property Tax Records by County

Each of South Carolina's 46 counties maintains its own property tax assessment and collection offices. Select a county below to find local resources, assessor contact information, and property tax search portals.

South Carolina Property Tax Records by City

City property taxes in South Carolina are administered through the county where each city is located. Select a city below to find property tax resources for that area.